Changes in the VAT treatment of certain supplies of hospitality, hotel/holiday accommodation and admission to certain attractions

A temporary VAT cut on from 20% to 5% for:

Food – eat in or hot takeaway food and non-alcoholic drinks, from restaurants, cafes and pubs

Accommodation - Hotels, B&Bs, campsites and caravan sites

Attractions – for example, cinemas, theme parks and zoos

When?

From Wednesday 15th July 2020 to Tuesday 12th January 2021.

“The temporary reduced rate will apply to supplies that are made between 15 July 2020 and 12 January 2021”

If the supply straddles the period of the VAT reduction, for example, payments have been received or invoices issued for supplies that will take place after 15th July 2020 there is specific guidance in sections 30.7.4 to 30.9.2 of VAT guide (VAT Notice 700) (see the section below for links).

Affected supplies

Food and non-alcoholic beverages sold for on-premises consumption, for example, in restaurants, cafes and pubs

Hot takeaway food and hot takeaway non-alcoholic beverages

Sleeping accommodation in hotels or similar establishments, holiday accommodation, pitch fees for caravans and tents, and associated facilities

Admissions to the following attractions that are not already eligible for the cultural vat exemption such as: Theatres, Circuses, Fairs, Amusement parks, Concerts, Museums, Zoos, Cinemas, Exhibitions, Similar cultural events and facilities. Note with regard to attractions, if the admission is covered by the existing cultural exemption then this will take precedence.

There are significant conditions/clarifications to whether the supply qualifies for the vat reduction, in particular the Catering, takeaway food (VAT notice 709/1) clarifies with regard to ‘catering services’ which remain standard rated. See the links on the following page for more detail.

Where a supply straddles the qualifying period, see sections 30.7.4 to 30.9.2 of VAT guide (VAT Notice 700) for guidance on the special provisions https://www.gov.uk/guidance/vat-guide-notice-700#changes-in-tax-rates-and-liability

Actions you may need to take in Microsoft Dynamics NAV/Business Central

After checking that the items/services you sell qualify for the VAT reduction then for all supplies of them within the date range (15th July 2020 to 12th January 2021) they need to be updated to use the newly reduced rate of 5%

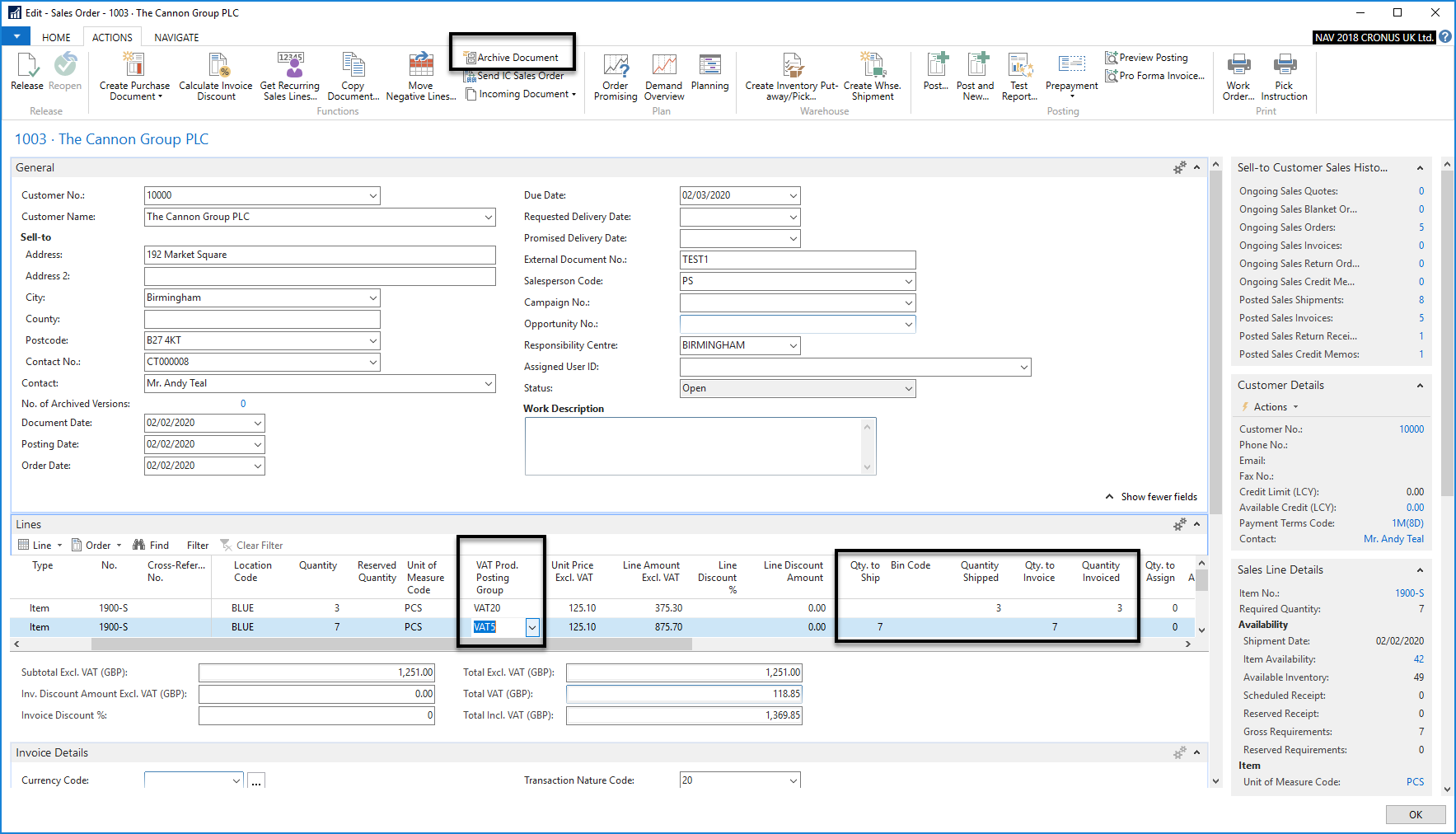

Please note the instructions below are accompanied by some images to assist on the following pages

Review all open orders, invoice all lines that have been supplied to date (using the existing/standard rate of 20%)

Update the VAT rate on the applicable products, for example, Items or GL codes to use the Reduced rate of 5% rather than 20%. This is done through the VAT Product Posting Group applied on the Card page. What this is called will vary between versions/companies but you usually already have one called Reduced or VAT 5 or something similar, you should not normally need to create a new rate.

For open orders with a remaining quantity, it may be necessary to split lines if it has been part shipped, to do this Reopen the Sales Order, reduce the quantity on the line to reflect what has been shipped to date, and ensure this has been invoiced. Then add in a second line for the same Item/GL for the remaining quantity/value and ensure that the VAT Product Posting Group that pulls through is the new correct one (i.e. the Reduced or VAT 5 one)

For open orders not yet shipped/supplied simply ensure the order status is Open (use Reopen) then change the VAT Product Posting Group on the relevant lines to use the reduced rate 5% setting (or delete and re-enter the lines)

The above points can be handled using the VAT Rate Change Tool (when used with appropriate filters)

Archive

For all of the above, it would be a good idea to create an Archive copy of the sales document for reference (using Actions – Archive Document in NAV or Actions – Functions – Archive Document in Business Central)

Please note, for most companies, No change is required to your VAT Posting setup – the required posting setup should already exist. Only if you have never sold a goods or service at Reduced rate / 5% will you need to create a new line in the Vat Posting Setup.

The above process assumes you are passing on the VAT reduction to your customer, so the final price they are to pay is being reduced and your item price is remaining the same.

If you wish to not pass on the VAT reduction, in effect increasing your sales price by the difference between 20% VAT and 5% VAT then this can be done. It would require a switch to the Item being set so that its Prices Include VAT (set on the Prices and Sales tab of the item card) and set the required unit price and update the VAT Product Posting Group (to VAT5 or equivalent).

Next steps

We have a document with more details on this process, please contact your account manager.